Now employers can offer a Health Savings Account (HSA) as part of their employees' Section 125 Cafeteria plan. Our CoreHSA Plan Document package makes it easy and affordable to expand employee options and reduce the cost of health coverage, all while maximizing tax savings for everyone. Also to know is, is an HSA a Section 125 plan?

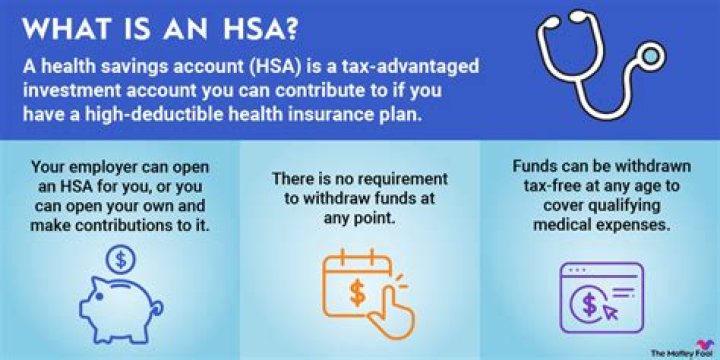

A cafeteria plan is an employee benefits plan administered under Section 125 of the federal tax code that lets employees pay certain expenses with pretax income. Funding a health savings account, commonly referred to as an HSA, may be an option under a cafeteria plan.

Furthermore, what are considered Section 125 deductions? Section 125 is the section of the IRS tax code where the items that can be deducted from employee pay on a pre-tax basis are defined. In the context of Section 125, “pre-tax” means that a deduction is exempt from Federal Income Tax Withholding, Social Security and Medicare Taxes.

Regarding this, is 401k part of section 125?

However, you can include certain types of 401(k) plans and life insurance plans maintained by educational institutions. Here are the qualifying benefits you can include in your section 125 cafeteria plan document: Accident and health benefits (not including Archer medical savings accounts) Adoption assistance.

Can you have an HSA and a cafeteria plan?

This is inexpensive and can be accomplished by adding a Section 125 Cafeteria plan with HSA deferrals as an option. Employers benefit by not having to pay payroll taxes on the employee's HSA contributions. Plus, HSA contributions are not counted as income for federal, and in most cases, state income taxes.

Related Question Answers

How do you set up a Section 125 plan?

To set up a Cafeteria Plan Employee payroll item with Custom Setup: - Choose Lists > Payroll Item List.

- Select the Payroll Item > New.

- Select Custom Setup > Next.

- Select Deduction > Next.

- Enter a name for your payroll item (for example, 125 Health Insurance Plan), and then select Next.

What is the difference between a cafeteria plan and a Section 125 plan?

A cafeteria plan, also known as a section 125 plan, is a written plan that offers employees a choice between receiving their compensation in cash or as part of an employee benefit. Who can set up a Section 125 plan?

Employers must hire and partner with a qualified section 125 third-party administrator, who can provide the most up-to-date documentation for plan setup and update the employer on the latest requirements necessary for compliance. What is the difference between a HSA and a cafeteria plan?

A cafeteria plan is an employee benefits plan administered under Section 125 of the federal tax code that lets employees pay certain expenses with pretax income. Funding a health savings account, commonly referred to as an HSA, may be an option under a cafeteria plan. How does a Section 125 cafeteria plan work?

Essentially, a Section 125 Cafeteria Plan allows an employee to reduce their gross income, effectively reducing the amount they pay in Federal, Social Security, and some State taxes. The employer also realizes savings on FICA withholding tax for each participating employee. Can an employer contribute to an HSA without a cafeteria plan?

Employers can make tax-free contributions to their employees' HSAs without using a Section 125 plan, as long as the contributions are "comparable" for all employees participating ("comparability rules"). What is Section 125 of the IRS code?

Section 125 is part of the IRS Code that allows employees to convert a taxable cash benefit (salary) into non-taxable benefits. Under a Section 125 program you may choose to pay for qualified benefit premiums before any taxes are deducted from employee paychecks. What is a 125 cafeteria plan?

What is a cafeteria plan? A cafeteria plan is a separate written plan maintained by an employer for employees that meets the specific requirements of and regulations of section 125 of the Internal Revenue Code. It provides participants an opportunity to receive certain benefits on a pretax basis. What are Section 125 benefits?

Section 125 is part of the IRS Code that allows employees to convert a taxable cash benefit (salary) into non-taxable benefits. Under a Section 125 program you may choose to pay for qualified benefit premiums before any taxes are deducted from employee paychecks. Is Section 125 required?

IRS Requirement for pre-taxed employee benefits. If you are an employer wanting to allow your employees to pay group health and other insurance premiums with pre-tax salary deductions, the answer is yes, you need a Section 125 plan document. However, that tax-advantaged treatment is not automatic. What is a Section 125 POP Plan?

A Section 125 Premium-Only-Plan (POP), is a cafeteria plan which allows employees to pay their health insurance premiums with tax-free dollars. Traditionally, these POP plans have been used in combination with employer-sponsored group health insurance plans. Is Section 125 pre tax?

Under a Section 125 program you may choose to pay for qualified benefit premiums before any taxes are deducted from employee paychecks. It allows for certain employee paid group insurance premiums to be paid with pre-tax dollars. The qualified premiums (if offered by employer) are: Health. Are 401k contributions exempt from FUTA tax?

Retirement/pension plan contributions made by the employer on behalf of employees to a qualified plan are exempt from FUTA tax. Such plans include: A SIMPLE retirement account. A 401(K) plan. What is a disadvantage of cafeteria style plans?

Employees who exceed their allocated spending amount pay a partial premium to their employer. So if Emma spends $1,000 over her allocated contribution, she pays a portion of that amount herself. The disadvantage of a cafeteria plan is it usually takes more time to administer and is typically more complex. What is Section 125 compliance testing?

The IRS requires non-discrimination testing for employers who offer plans governed by Section 125. This means any plans that allow employees to contribute pre-tax income into a benefits account, such as a Flexible Spending Account (FSA). What is Section 125 on a w2 form?

SEC 125 is your employer's benefit plan. It is also known as a "cafeteria plan". Usually, what is reported there is your medical insurance premiums that are paid with pre-tax income. They are not taxed and are not included in your W-2 Box 1 wages so you can not deduct them as medical expenses. Does Section 125 go on w2?

Under a cafeteria, or Section 125, plan, you pay for your employer-sponsored benefits with pretax money. Your employer doesn't include your pretax payments in your taxable wages on your annual W-2. It may, however, choose to report certain benefits on your W-2 and code them as Café 125. Is a cafeteria plan worth it?

Cafeteria plans are particularly good for participants who have regular expenses related to medical issues and child care. Employees enrolled in a section 125 plan can set aside insurance premiums and other funds pretax, which can then be used on certain qualified medical and child care expenses. Does an HSA require a plan document?

All the IRS requires for tax-advantaged treatment of Cafeteria plans – including a Health Savings Account – is that a written plan document be completed by and on file with the employer. Employers with an existing Section 125 plan document must update it to include the HSA and any new limited FSA options. Why is it called a cafeteria plan?

Its name comes from the earliest such plans that allowed employees to choose between different types of benefits, similar to the ability of a customer to choose among available items in a cafeteria. Qualified cafeteria plans are excluded from gross income. What are HSA contributions through a cafeteria plan?

A Cafeteria Plan is a reimbursement plan governed by IRS Section 125 which allows employees to contribute a certain amount of their gross income to a designated account or accounts before taxes are calculated. Is an HSA an Erisa plan?

An HSA is not an ERISA plan simply because the employer pays HSA fees that the employees otherwise would have to pay. Employers may limit the HSA providers allowed to market their HSA products in the workplace or may select a single HSA provider to which it will forward contributions without triggering ERISA coverage. What is an example of a cafeteria plan?

A flexible spending arrangement (FSA) is also a common cafeteria plan benefit. Company XYZ contributes money to the cafeteria plan by taking deductions from employees' salaries (those who participate in the plan). Those deductions are not subject to FICA or unemployment taxes. Does a cafeteria plan reduce Social Security?

Your payroll deductions for your cafeteria plan benefits are done on a before-tax basis. Qualified benefits are not subject to federal income tax, Social Security tax, Medicare tax and, in most cases, state income tax. This process may cause a slight reduction in your Social Security benefits when you retire. Are cafeteria plan benefits taxable?

Generally, qualified benefits under a cafeteria plan are not subject to FICA, FUTA, Medicare tax, or income tax withholding. Adoption assistance benefits provided in a cafeteria plan are subject to social security, Medicare, and FUTA taxes, but not income tax withholding. Are HSA contributions pre tax for FICA?

According to IRS guidance, "The employer contributions [to an HSA] are not subject to withholding from wages for income tax or subject to the Federal Insurance Contributions Act (FICA), the Federal Unemployment Tax Act (FUTA), or the Railroad Retirement Tax Act." As a post from Tango Health clarifies, "A pretax